While I have gone on record as saying that the PBM rebate-contracting commercialization model is badly broken, in 2023, we saw in rapid succession each of the big three branded insulin suppliers abandon that sales model.

While many lawmakers are now telling everyone that it was the passage of the Inflation Reduction Act (IRA) which helped bring insulin prices back down to earth, the thing is, unless you are on Medicare, the IRA had almost NO impact on insulin prices so far.

In fact, it was really the passage of the American Rescue Plan Act (ARP) of 2021 which is helping to bring U.S. insulin prices down for everyone not on Medicare. On top of that, the Inflation Reduction Act contained a toxic provision which EXTENDED the safe-harbor exemption for rebates paid to Pharmacy Benefit Managers (PBMs) from prosecution for bribery under the federal Antikickback Statute until Jan. 1, 2032 (the House version of that bill was only until Jan. 1, 2027, but upon reconciliation with the Senate version of the bill, another five years were added). That was a very bad thing. Lawmakers did that in order to boost the Congressional Budget Office (CBO) score given to the Inflation Reduction Act. But it also threw anyone covered under employer-sponsored commercial healthcare insurance plans under the bus.

The Kaiser Family Foundation had an excellent overview of exactly how American Rescue Plan of 2021 impacted many older but heavily-rebated drugs including insulin which can be read at https://www.kff.org/policy-watch/what-are-the-implications-of-the-recent-elimination-of-the-medicaid-prescription-drug-rebate-cap/.

To get around the problem which Novo Nordisk had helped to perpetuate, in 2022, the company quietly introduced an unbranded (sold under the generic drug name) version of its basal insulin Tresiba since it had already seen success with an unbranded version of Novolog which reportedly reached more than 1 million American patients according to the company's annual report (see the company press release HERE for details on the launch of Novo Nordisk's unbranded version of Tresiba). A photo of the vial form of that insulin is pictured below.

But with the unbranded product offerings being so successful without much in the way of marketing, combined with the Civica/CivicaScript-JDRF biosimilar insulin announcement which arguably set a ceiling on biosimilar insulin prices, those things essentially FORCED Lilly, Novo Nordisk and Sanofi collectively to simply abandon the rebate-contracting sales model for insulin, and those 70%+ price cuts were accomplished with zero impact to the manufacturers' bottom lines; they did so by disintermediating the legally exempted rebate kickbacks (bribes) paid to PBMs for exclusive formulary placement. I've covered that at various times recently, but one post summarized it nicely at https://blog.sstrumello.com/2023/06/what-happens-when-rx-price-bubbles-such.html.

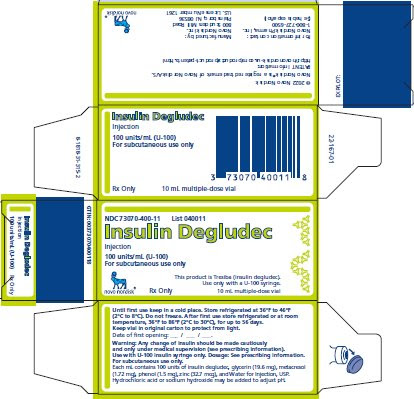

Anyway, at the 23rd Annual Needham Virtual Healthcare Conference which took place on April 8-11, 2024, we learned from Amphastar Pharmaceuticals that the company has been expanding its diabetes business in recent years. If you visit slide #15 (see the presentation at https://ir.amphastar.com/download/companies/270152a/Presentations/Needham.pdf for more), we see Amphastar has a biosimilar of insulin aspart (fka Novolog) currently pending an FDA approval decision. For the company's aspart biosimilar, the company previously told investors it had received an FDA "Complete Response Letter" which means it was not approved, but upon addressing FDA-cited deficiencies, it will be able to resubmit that for approval (hence the designation "AMP-004m"). The slide indicates the resubmission was "in progress" as of April 8, 2024. But also look at what I circled in the image below taken from one slide of that that particular investor presentation.

But we also learned that it has now has biosimilars not only of insulin aspart, as well as regular insulin (the innovators are branded as Humulin R or Novolin R), with a version of 100 units/mL (U-100) as well as a version with 500 units/mL (U-500) for which Lilly's U-500 Humulin R insulin had quietly become a bestseller thanks to growing incidence of Type 2 diabetes patients with very high insulin requirements.

In addition to those, we also learned that Amphastar also has a copy of insulin degludec, better known by its brand-name Tresiba from Novo Nordisk. I mistakenly believed that Tresiba had patent protections still remaining. While I thought it had patent protections until 2032, according to the U.S. Patent and Trademark Office (see https://www.uspto.gov/patents/laws/patent-term-extension/patent-terms-extended-under-35-usc-156 for more), it reports that insulin degludec patent terms (which were extended already) will officially expire on July 22, 2024 which is about 8 years of patent exclusivity.

Overall, branded insulin manufacturers secured a median of 16 years of protection on their insulin products through patents and exclusiveness, surpassing the median of 14 years observed in other studies of top-selling small-molecule drugs. Keep in mind that insulins were regulated and approved as small molecule drugs at the time and that Tresiba was approved in 2016 as a "drug". Some of the most widely used insulins, such as glargine and degludec, were among those with the longest periods of market exclusivity. (refer to https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10653475/pdf/pmed.1004309.pdf for the published paper which reported this). We know that FDA first approved Tresiba (insulin degludec) in 2016.

Regardless, we know with absolute certainty that Novo Nordisk's second attempt at a "Lantus killer" known as Tresiba was expected to be its winner, but without legally-exempted rebate kickbacks paid to vertically-integrated (with commercial healthcare insurance companies) Pharmacy Benefit Managers ("PBMs"), Tresiba never really killed Lantus, and now no fewer than about 4 more biosimilar copies of insulin glargine expect approval decisions in 2024 (in addition to the two already on the market). And, thanks to the FDA revised policy decision on insulins which went into effect in 2020, the approved marketing applications for the small subset of "biological products" (medicines) including insulin and human growth hormone – which for complex historical reasons were previously generally approved as drugs under section 505 of the FD&C Act – will be deemed to be biologics licenses under section 351 of the PHSA. That meant these products, even though approved as "drugs" would be recognized as biologics and therefore eligible for biosimilars and governed as such.

For its part, Novo Nordisk had hoped its once-weekly basal insulin to be branded as Awiqli (pronounced like "A Weekly") known generically as icodec insulin injection would help it win in the basal insulin market. But that was dealt a severe blow by the FDA on May 28, 2024 when the FDA's Endocrinologic and Metabolic Drugs Advisory Committee voted against the approval of Novo Nordisk's once-weekly insulin icodec injection for Type 1 diabetes. The FDA's internal reviewers flagged its risk, noting in its briefing document https://www.fda.gov/media/178821/download that while hypoglycemia is an expected side effect of insulin products generally, insulin icodec did not yield "additional glycemic control or other benefit" in Type 1 diabetes patients. In a 7-4 vote, the panel of external experts found that insulin icodec's benefits do not outweigh its risks. That also means that the Awiqli product would not be FDA approved by the vast majority of U.S. insulin users who have Type 1 diabetes (Type 2 patients use significantly more insulin, but are fewer in number than Type 1 patients).

In particular, there were serious concerns about how emergency personnel would deal with the inevitable insulin icodec overdoses. For patients with Type 1 diabetes, a weekly basal insulin was described by some commenters as "a solution in search of a problem to solve" since it did nothing to mitigate a need for injected prandial insulin.

The bottom line is this: we now have biosimilars for the basal insulin Lantus already on the market with a whole bunch more coming soon, plus the basal insulin Tresiba, as well as for the prandial insulins Novolog, Humalog and even the old-school rDNA Regular insulin (with the 500 units per mL or "U-500" version expected to be the bigger seller compared to the less concentrated U-100 version) all coming to market soon. That explains why Novo Nordisk tried very hard to extend its GLP-1 patents to get an extra 30 months by inappropriately listing injector devices in the FDA Orange Book (which was illegal, incidentally). But the Federal Trade Commission noticed those patents and filed a complaint with the FDA about how those patents did not belong in the Orange Book, meaning copies of patent-expired liraglutide (fka Novo Nordisk Victoza/Sexenda) are now already on the market (Teva's authorized generic is the first, but even more are expected to receive FDA approval decisions later this year, and permitted to come to market after December 26, 2024, meaning they'll hit the market soon after the New Year).

No comments:

Post a Comment